The efficient market hypothesis (EMH) seems to have numerous definitions, but the general idea is that the current prices in a market (such as a stock market) reflect all available information, and that, therefore, you can’t make risk-adjusted profits in excess of the (purely theoretical) risk-free rate of return by (for example) analysing the past prices of stocks and anticipating their future movements.

The intuitive idea is this: if anyone could easily predict future prices of stocks, they would do so and attempt to profit by buying stocks that are likely to rise, and selling stocks that are likely to fall. But by doing so, such people would bid up the value of stocks that will rise, and bid down the value of stocks that will fall, moving their prices to the prices they’re predicted to have in future. So the present price should reflect the expected future price.

So if the EMH predicts that expected excess profits are impossible, it certainly predicts that guaranteed excess profits are impossible, which poses a puzzle when considered alongside this surprising guarantee.

When considering this puzzle, I decided that its solution may lie in the point of view from which the EMH is considered. Do people want to maximize their expected wealth as measured in dollars, or as measured in euros?

Of course, rational people would be more likely to want to maximize the expected utility now and in future from their spending of time and wealth, but utility is difficult to measure, except by assuming that people act in the best interests of their own expected utility when deciding whether to spend money now or save it for later. For this reason, we can simplify things by looking at people’s uses of a convenient currency, bearing in mind that money now is almost certainly worth more to someone that the same amount of money later, since the former can be used for anything the latter can be used for (by holding onto it and waiting), but the reverse isn’t true.

This article considers a simplified version of the EMH, and proves that it results in nonsense (and therefore either it must be an over-simplification of the EMH, or the EMH itself is nonsense).

There are, in fact, several simplifying assumptions made:

- that currency trades involve no transaction costs,

- that at any given point in time, there’s a single exchange rate at which two given currencies can be traded in either direction (that is, that bid–offer spreads are negligibly small),

- that the exchange rate will remain positive with probability

,

- that money can be borrowed or invested at a known risk-free interest rate (which also acts as a way of taking into account the point made earlier that money now is worth more than money in the future), and

- that markets are efficient from the point of view of risk-neutral traders.

To understand the last assumption, suppose someone offers you either $1 (with certainty) or $2 (with a probability of 50%). Which would you prefer? If you’re indifferent, then you’re risk-neutral; if you’d prefer the certainty of a dollar, you’re risk-averse; and if you’d prefer the chance of $2 (perhaps for the excitement of the gamble, or because you want something expensive that $1 alone can’t get you), then you’re risk-seeking.

There’s also one complexifying assumption that I haven’t seen considered elsewhere: that the currency-trading market is efficient both from the point of view of someone wishing to maximize their expected number of dollars, and from the point of view of someone wishing to maximize their expected number of euros. (Of course, you can substitute any two currencies you like.)

Suppose that a dollar buys

It’s tempting to say that

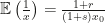

If the efficient market hypothesis holds from the point of view of the risk-neutral dollar-user, then the value of a dollar invested at the risk-free rate should be the same as the expected value if it’s converted to euros, invested at the euro risk-free rate, and then converted back at the later exchange rate. In symbols:

Going through the same reasoning from the risk-neutral euro-user’s point of view, we have

At first glance, this may look unsurprising; it may seem reasonable that if

Each term simplifies to

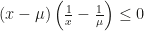

But hold on: since

That is, the future exchange rate is almost certainly known in advance.

So if your model of the currency markets makes the assumptions I've made above, and if it further assumes that exchange rates are not completely predictable, then you'll be able to prove anything you like, and it'll mean nothing at all.

I don't think this is a fatal blow to every form of the EMH, especially given its intuitive appeal; after all, there's no such thing as a free lunch. But if the EMH is true, then one of the assumptions must be at fault.

Perhaps I'll try to check this in more detail one day, but my intuition is that removing the assumptions about transaction costs, spreads, and so forth, might explain a little volatility in exchange rates, but not as much as there is in real life; my intuition is that the fault is with the assumption that it applies to risk-neutral traders.

Now there are models that assess markets in detail from the point of view of risk-averse traders, such as the Capital Asset Pricing Model, so what I’m saying won’t overturn the theories of everyone who relies on the EMH; take it only as a warning not to over-simplify the EMH (which would be easy to do on a naïve reading of Fama (1998), who says that the “simple market efficiency story” is that “the expected value of abnormal returns is zero”, but perhaps it turns on the interpretation of “abnormal”).